Author: Menno Jansen, Project Consultant at TriFinance

![]()

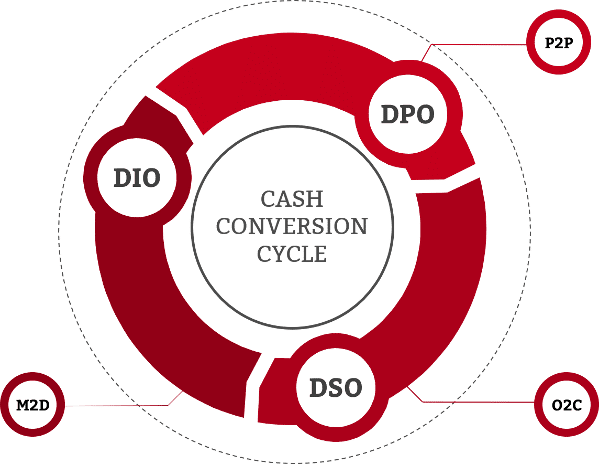

Before we proceed to make an overview, we first need to address the Cash Conversion Cycle again. The Cash Conversion Cycle consists of three processes: Order-to-Cash (Accounts receivable & work in progress) with DSO (Days Sales Outstanding), Make-to-Delivery (Inventory) and Purchase-to-Pay (Accounts payable) with DIO (Days Inventory Outstanding) and DPO (Days Payables Outstanding) respectively as key performance indicators.

Figure 1: The Cash Conversion Cycle, consisting of DPO, DSO and DIO, where the DSO is related to the O2C process (Order-to-Cash), DPO to P2P (Purchase-to-Pay) and DIO to M2D (Make-to-Delivery).

The following chart shows examples for each process or process steps that can, directly or indirectly, be influenced by the finance department. A distinction could also be made between those finance departments that depend on a shared service center. However, here we are considering the entire finance organization.

| Working Capital Position | Exercising Direct Influence | Exercising Indirect Influence |

| Accounts receivable & work in progress (O2C) |

|

|

| Stock (M2D) |

|

|

| Credits (P2P) |

|

|

The forgotten link

The overview above shows that few subjects can be influenced directly by the controller. Even for many of the actions that lie within the direct sphere of influence, the controller still has to work together with their colleagues from other departments. This means that, in our position as controllers, we are most effective when we are able to exercise influence on the working capital from outside our own direct sphere of influence.

In other words: you need your colleagues to ensure both a solid working capital management and to meet your cash targets. For this to be a success, your skill level when it comes to influencing the behavior of others, motivating them and getting them to make an effort to improve the working capital is vital. Influencing your colleagues and customers is the oft-forgotten link in the chain of working capital management. Our next blog will tell you which tools to use for this.